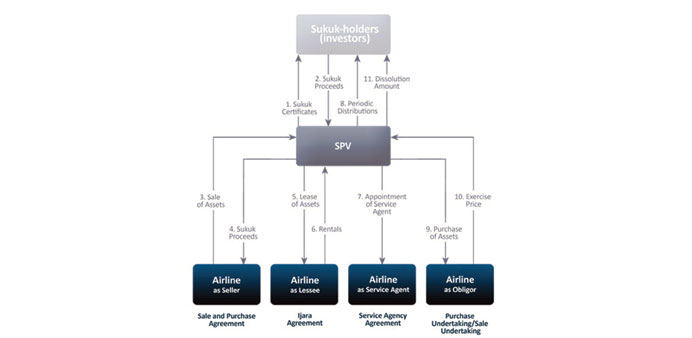

A basic ijara sukuk structure for airline leasing or purchasing. SPV is a “special purpose vehicle,” a financing company that acts as facilitator. Source: AviaAM Leasing.

By Arno Maierbrugger

Gulf Times Correspondent

Bangkok

The launch of a fully Shariah-compliant airline in Malaysia last Sunday, Rayani Air, has put one particular aspect of Islamic finance back into the limelight: Islamic airline financing. Over the past years, and particularly after the global financial crisis of 2007-08, there was a recovery in the use of sukuk as an alternative source of funding for companies in the aviation sector. A number of international airlines tapped the Islamic capital market through different types of sukuk to fund the purchase or leasing of aircraft, among them Emirates, Etihad Airlines, Saudi Arabian Airlines, Air Arabia, Royal Jordanian, Pakistan International Airlines, SriLankan Airlines, Garuda Indonesia, Malaysian Airlines, Turkish Airlines, Ethiopian Airlines, AirAsia and even GE Capital Aviation Service (GECAS), the world’s largest aircraft leasing company.

In 2014, a new financing company, International AirFinance Corp, entered the market together with Airbus and the Islamic Development Bank and launched a $5bn Shariah-compliant aircraft leasing fund. It was the first time that a financing company for aircraft completely utilised Islamic financing structures. Planemaker Airbus developed the fund together with two Dubai-based financial institutions, Quantum Investment Bank and Palma Capital, and is seeding it jointly with the Islamic Development Bank. Saudi Arabian Airlines this June was one of the first to tap the fund in its largest ever aircraft leasing deal to acquire 30 Airbus planes and lease another 20 aircraft.

“We came very quickly to the conclusion that asset-based finance is very attractive under Islamic finance principles,” said Yann Ballet, head of project and structured finance at Airbus maker EADS.

And the business is huge, especially in the Gulf countries and the South and Southeast Asian aviation market. Gulf airlines such as Etihad Airways, Emirates and Qatar Airways have transformed the aviation industry over the last decade through aggressive expansion, while Islamic finance is a growing element to win business in the region.

And in South and Southeast Asian, population growth and increased demand for air travel keeps dozens of budget carrier hunting for financing to expand their fleets, and many discover Islamic financing to best suit their needs.

Commercial aircraft financing was above the $100bn-mark in 2014, whereby lease financing currently represents a third of aircraft deliveries. This share could reach half of all new aircraft deliveries by the middle of the next decade, industry analysts say.

Islamic finance is especially attractive to the aviation industry through its asset-back financing structure, whether for purchase or for leasing. But how does it work? While, under conventional financing methods, the lessee pays a monthly rental fee in advance plus regular maintenance payments to compensate the lessor for the maintenance utility consumed by the lessee, under a Shariah-compliant financing structure, the lessor remains responsible for maintenance, equipment and ownership taxes. But In practice, neither the Islamic financier nor the airline would want the financier to be responsible for these things. Usually, the lessor appoints the airline lessee as its service agent and pays for it. The lessor, as principal, must repay the service agent these costs. Normally an amount equal to that repayment obligation is added as extra rent. The repayment obligation and the extra rent are set off. The economic liability passes to the lessee, but in a Shariah-compliant manner.

In many cases, an ijarah structure is used for this type of financing. An ijarah contract is quite equivalent to a conventional lease agreement and is therefore a popular choice in Islamic aircraft financing. Some of the basic principles in an ijarah contract are, amongst others, that the asset has to be of valuable use, that all risk of ownership is borne by the lessor and all liabilities arising from the use of the asset is borne by the lessee.