Consumption is one of the major engines of the US economy. Expenditures by households account for approximately 68% of GDP, and thus represent the most vital segment of the US economy. Therefore, it provides important information regarding the outlook of the overall economy, and of the likelihood of a soft or a hard landing, QNB stated in its latest economic commentary.

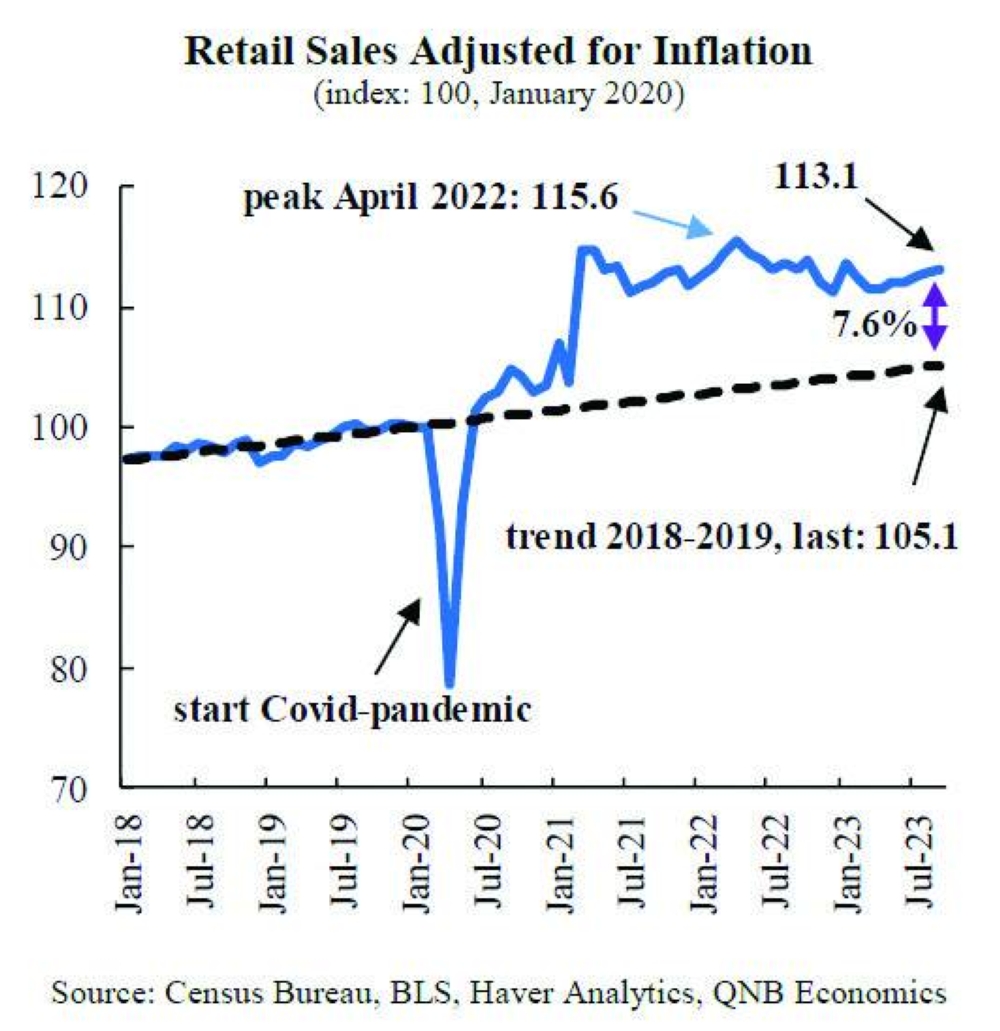

The latest release of the national accounts for Q3-2023 showed its exceptional performance, expanding at an annual rate of 4%. To put this number into perspective, it is significantly higher than the 2.6% average in the five years before the Covid-19 pandemic. Similarly, retail sales adjusted for inflation have grown continuously since May, and remain 7.6% above their pre-pandemic trend, showing little signs of a slowdown.

“But what is supporting these exceptional levels of consumption? And how much longer can the US households keep up with this pace? In this article, we discuss two main factors that will continue to support consumption in the coming months,” QNB stated.

First, households have abundant resources to continue spending and a strong balance sheet that will continue to support consumption. During the Covid-19 pandemic, households built up savings at an extraordinary rate.

This was a result of the closures and social distancing measures that constrained usual spending patterns, together with the government stimulus packages that injected $5tn into the economy.

During the Covid-19 pandemic, between March 2020 and August 2021, the stock of “excess savings,” defined as the unusual accumulation of wealth above the pre-pandemic trend, reached approximately $2.1tn. These funds provided a persistent boost to consumption. Going forward, additional factors will add to excess savings to sustain the surge in spending, QNB stated.

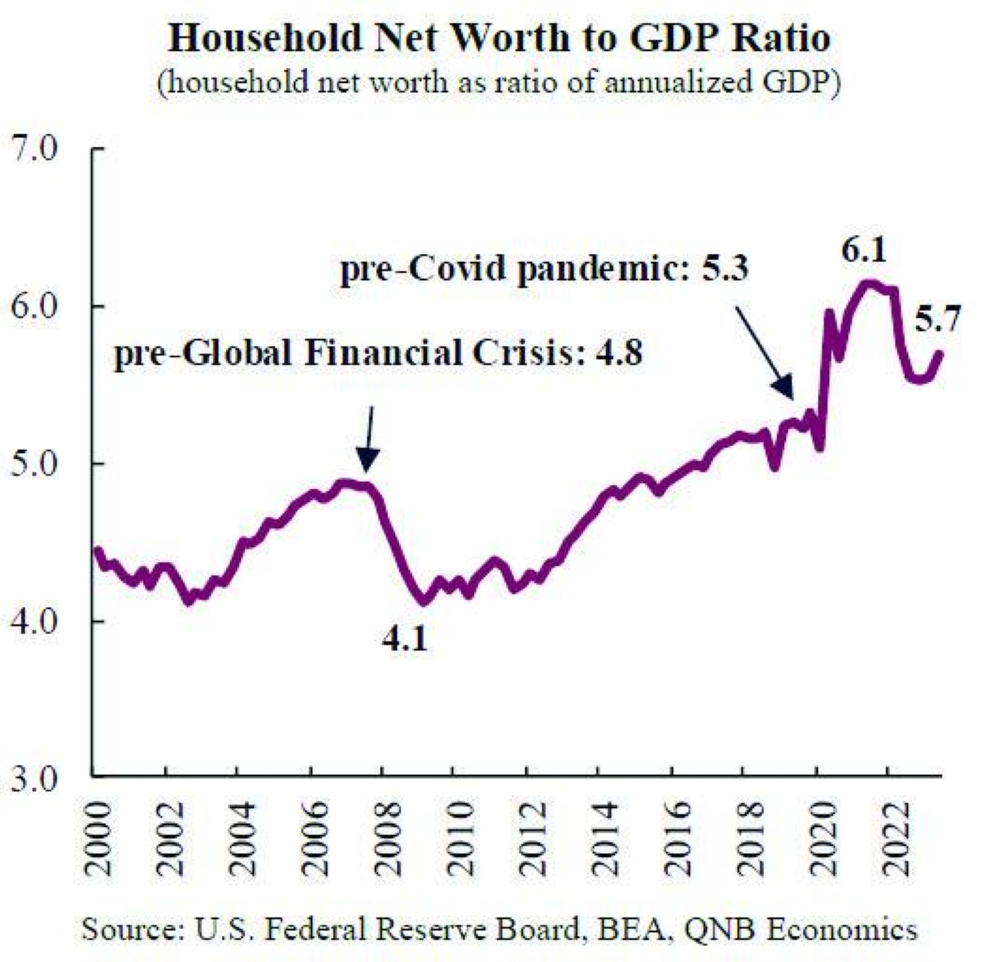

The Household Net Worth (HNW) statistics provide valuable information regarding assets and liabilities for an assessment of the US household balance sheet. In Q2-2023, the net worth of households increased by $5.5tn, reaching $154.3tn. This was mostly due to continuous capital appreciation from equity and real estate holdings, QNB stated.

When expressed as a ratio of GDP, current levels of net worth are historically high, showing the solvency of American families. Absent a major correction in asset prices, the strong wealth effect and abundant available resources will continue to support resilient consumption.

Second, labour markets remain tight and indications of weakening are still modest relative to the distinctive warning signals of a recession. The latest release of the unemployment rate stood at 3.9%, which shows some gradual softening relative to the minimum of 3.4% this year, but is still robust in historical comparison, QNB stated.

In general, labour markets can deteriorate either because existing jobs are being eliminated at a faster rate, or if firms are creating new positions at a slower pace. Although job gains have moderated this year, they still continue to sustain a steady pace. In the last three months, nonfarm payrolls added an average 204,000 jobs per month, still slightly above the 150-200,000 range that is typically considered in line with a healthy rate of job creation, and higher than the pre-pandemic average of 177,000 during 2018-2019.

In terms of job destruction, the data from the Job Openings and Labour Turnover Survey (JOLTS) shows a downward trend this year, while initial claims of unemployment insurance remain stable. Thus, labour markets remain supportive of household consumption, QNB stated.

“All in all, we expect US consumption to remain firm in the coming months. The household balance sheet continues to provide a boost given positive wealth effects and the availability of funds for spending, while labour markets continue to offer abundant jobs. Given the importance of consumption, this reduces the likelihood of a sharp downturn in the US economy,” QNB stated.

Business

What explains the sustained strength of US consumer spending?

US consumption to remain firm in coming months: QNB