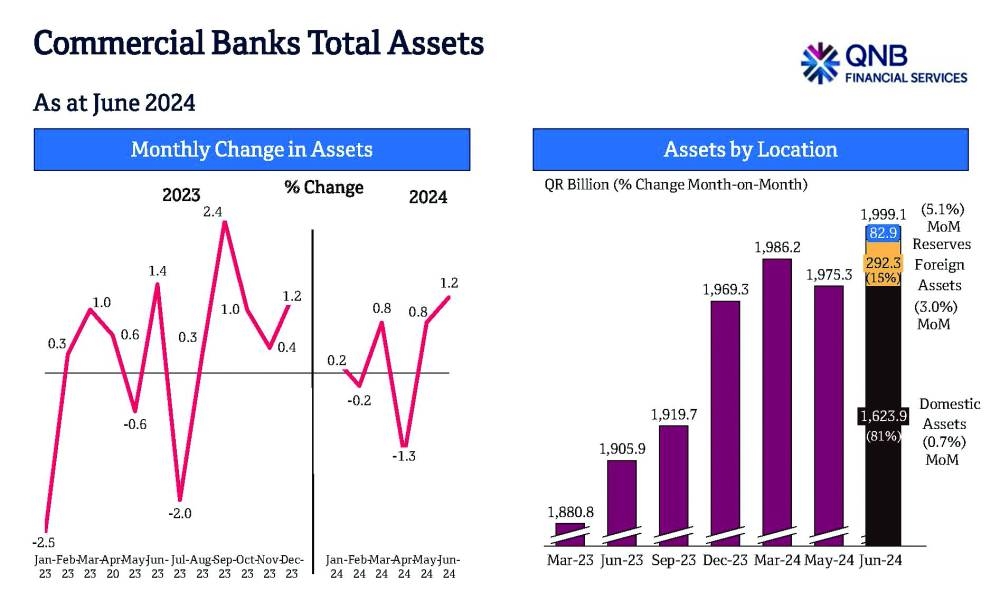

Qatar’s banking sector assets rose 1.2% month-on-month (m-o-m) and (1.5% so far in 2024) to QR1.999tn in June, mainly due to the increase in both domestic credit and domestic investments, according to QNB Financial Services (QNBFS).

Total assets were up 1.5% in 2024, compared to a growth of 3.4% in 2023. Assets grew by an average 6.8% over the past five years (2019-2023), QNBFS said in its ‘Qatar monthly key banking indicators’.

Liquid assets to total assets moved higher to 30.7% in June, compared to 30.1% in May this year.

Bank loans moved up by 0.4% during June to reach QR1,324.8bn.

The loans increase in June was mainly due to gains (by 0.7%) in the private sector, particularly in the services segment.

Loans increased by 2.9% in 2024, compared to a growth of 2.5% in 2023, while loans grew by an average 6.5% over the past five years (2019-2023).

Loan provisions to gross loans was at 4.1% in June, compared to 3.9% in May.

Deposits edged marginally down during June to QR1,031.8bn due to a drop by 2.4% in public sector deposits, even as non-resident deposits surged by 4.3% in June.

Deposits increased 4.6% in 2024, compared to a decline by 1.3% in 2023. Deposits grew by an average 4.1% over the past five years (2019-2023).

With deposits marginally declining in June, the loans to deposits ratio (LDR) went up to 128.4%, compared to 127.9% in May.

According to QNBFS, the services sector was the main driver for the second consecutive month, pushing up the private sector loans in June.

Services (contributes 32% to private sector loans) gained by 1.3% m-o-m (3.7% in 2024), while the real estate segment (contributes 20% to private sector loans) increased by 1% m-o-m (+4.3% in 2024) and general trade (contributes 22% to private sector loans) edged up by 0.2% m-o-m (+3% in 2024).

However, consumption and others (contribute 20% to private sector loans) declined by 0.8% m-o-m (-3.3% in 2024) in June.

Total public sector loans moved marginally up m-o-m (3.8% in 2024) in June. The government institutions’ segment (represents 66% of public sector loans) was the main driver for the public sector with an increase by 0.6% m-o-m (+4.7% in 2024), while the semi-government institutions segment went up by 1% m-o-m (-9.1% in 2024).

However, the government segment (represents 29% of public sector loans) declined by 1.4% m-o-m (4.5% in 2024) in June.

Outside Qatar loans dropped by 1.8% m-o-m (12.9% in 2024) in June.

Public sector deposits fell by 2.4% m-o-m (7.1% in 2024) in June, driving the overall marginal decline in deposits.

Looking at segment details, the government institutions’ segment (represents 56% of public sector deposits) dipped 3.2% m-o-m (6.4% in 2024), while the semi-government institutions’ segment went down 2.8% m-o-m (-13.9% in 2024) and the government segment (represents 32% of public sector deposits) moved lower by 0.9% m-o-m (19.8% in 2024) in June.

Private sector deposits made a marginal gain of 0.1% m-o-m (+0.8% in 2024) in June 2024. The companies and institutions’ segment moved up by 0.6% m-o-m (-4.3% in 2024). However, the consumer segment edged down by 0.3% m-o-m (+5.3% in 2024).

Non-resident deposits jumped by 4.3% m-o-m (+10.0% in 2024) in June.

The banking sector's loan provisions to gross loans was at 4.1% in June, compared to 3.9% in May 2024. Liquid assets to total assets moved higher to 30.7% in June, compared to 30.1% in May 2024.

An analyst told Gulf Times, “The key highlights for the month of June are the increase in total assets by 1.2%, which rose mainly due to the increase in both domestic credit and domestic investments (on the domestic assets side) and a spike in due from banks abroad on the foreign assets side.

“The 0.4% increase in the overall loan book resulted mainly from a 1.3% gain in June from the services segment, signifying the further strengthening of tourism sector. Even as overall deposits were marginally down for the month, non-resident deposits witnessed a significant rise by 4.3% in June.”

Classified

Qatar’s banking sector assets rise 1.2% month-on-month to QR1.999tn in June: QNBFS