Germany’s real GDP is expected to remain unchanged in 2024 and average 1% growth in the next several years, according to QNB.

“This is an underwhelming performance as the economy faces significant hurdles from the negative trends in the industrial sector, inadequate infrastructure, and loss of competitiveness.

“Importantly, this is not only a result of cyclical weakness, but a secular trend that would require deep policy changes for a turnaround and the return of healthier growth rates,” QNB said in an economic commentary.

Historically, Germany was portrayed as the epitome of high productivity, displaying superior engineering expertise and a strong work ethic.

Not surprisingly, Germany has also acted as the economic powerhouse of Europe during extended periods of time, including the post-World War II recovery and after the country’s unification.

However, over the last couple of decades, several headwinds started to mount. These included negative demographic trends, red tape, policy missteps, an inability to upgrade leading manufacturing sectors and adapt to the digital age.

As a result, Germany’s economy started to underperform in recent years, to the point where the country has even been referred to as the “sick man of Europe”, QNB noted.

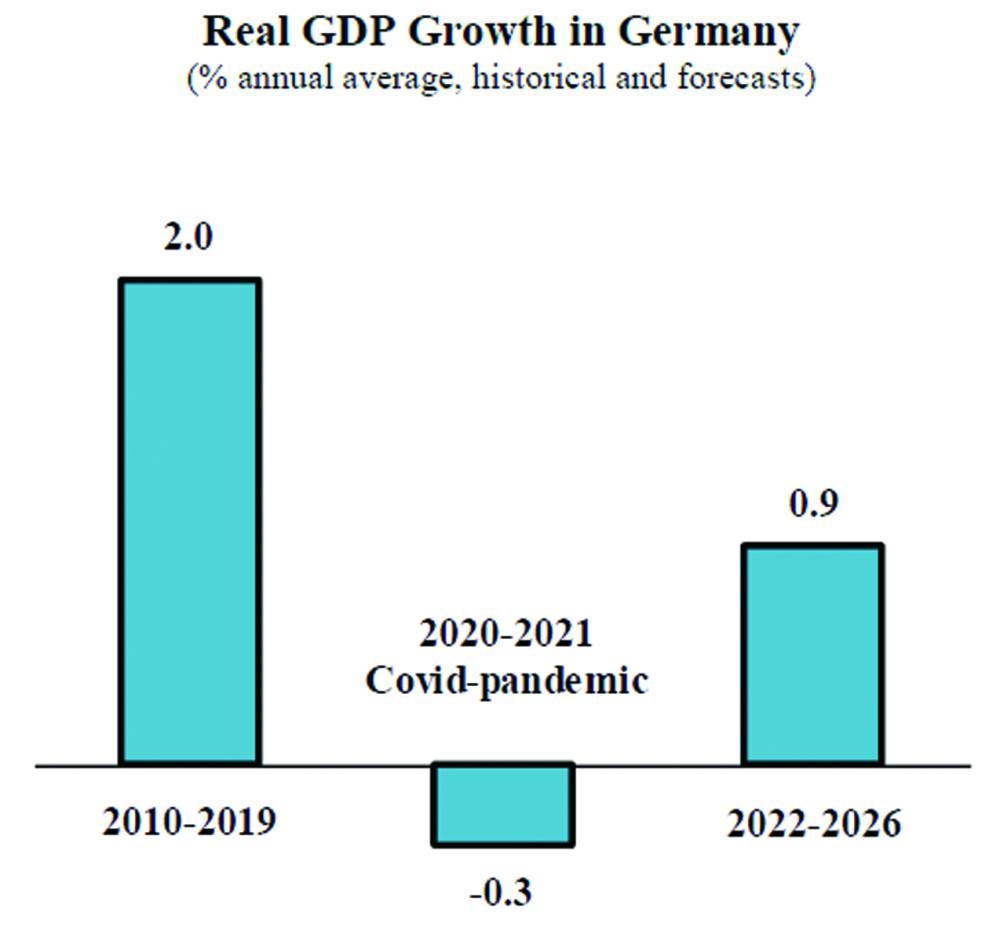

Since Q4-2019, the last quarter before the Covid pandemic began to unleash its impact globally, Germany’s real GDP has remained practically unchanged.

Five years of lost economic growth is not a minor setback in a rapidly evolving context where the world economy is expanding at an average rate of 3% per year.

Furthermore, on an accumulated basis, it compares poorly with the 9% expansion for the US, or even the 5% growth for the rest of the Euro Area during the same period.

For the 2022-2026 period, economic growth in Germany is expected to average 0.9% per year, much below the pre-pandemic average of 2%.

Understanding Germany’s economic stagnation requires an analysis of external and internal conditions, as well as cyclical and structural challenges, QNB said.

In this article, QNB analyses three key factors that explain Germany’s economic underperformance.

First, the manufacturing sector, once a pillar of Germany’s successful development story, is extending a sustained period of decline and has turned into a drag for growth. More than in most countries, manufacturing is a key sector in Germany, where it has represented close to 22% of GDP in recent years.

This weight increases to approximately 35% when taking into account its impact on other sectors, spanning from raw materials to services, such as logistics and financing.

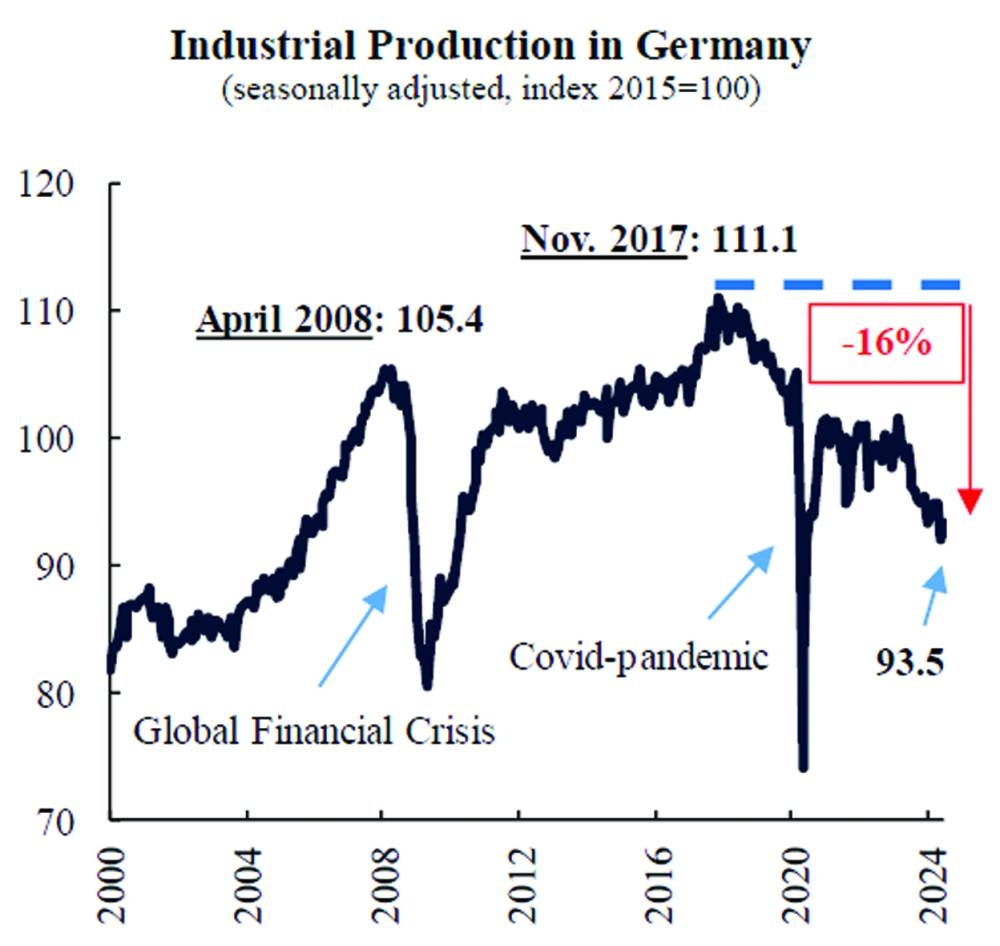

Historically, between 2000 and the peak in 2017, the industrial component of real GDP grew at an annual rate of 1.9%. This robust pace reversed dramatically afterwards, and its contribution to GDP growth turned negative as the sector faced a successive series of negative shocks.

Adverse events included escalating global trade tensions, a slowing world economy, the Covid-pandemic, a severe shortage of semiconductors, and the energy crisis due to the Russo-Ukrainian war (to which Germany was particularly vulnerable given its reliance on Russian gas).

Since its peak in 2017, industrial production accumulates a contraction of 16%, a striking divergence with the 1.7% growth for the US, or even the 2% decline for the rest of the Euro Area during the same period.

Automobile production, one of Germany’s flagship industries, is impacted by a shift of consumer preferences towards electric vehicles, stricter environmental regulations, and a shortage of skilled workers.

Automobile production has fallen by 28% from the 471 thousand units per month in 2017 to 337 thousand in 2024. This is a significant challenge to the economy, given that the automotive manufacturing represents 5-7% of GDP in Germany, compared to 2-3% in the US and France. Given the importance of manufacturing, these trends are dragging the performance of the German economy.

Second, conservative fiscal policy has led to an underfunding in key infrastructure areas, such as transportation, digital technology and energy, contributing to the decline in economic growth. Germany’s commitment to fiscal discipline is embodied in rules such as ‘Schwarze Null’ (Black Zero), which target a balanced budget without incurring new debt.

As a result, the public balance sheet in Germany is one of the strongest amongst major advanced economies. The ratio of public debt to GDP is 64% and falling, in contrast to the levels of 122% and 112% for the US and France, respectively.

However, fiscal discipline has come at a cost in terms of low levels of public investment, which in 2023 fell to 2.6% of GDP, compared to 4.1% in France, for example.

As a result, ageing infrastructure for transportation and energy, and lagging digital technology are hindering long-term economic growth.

Third, the economy faces significant institutional challenges that continue to erode German competitiveness and productivity. The World Competitiveness Report provides a useful assessment of competitiveness across countries.

Just a decade ago, Germany was ranked 6th in the world. However, since then, the country dropped markedly in the rank to the 24th position this year, QNB said.

The report sheds light on key issues that explain the decline, highlighting burdensome tax policy and business legislation. The “rigidity” of labour markets is another source of concern, given strong employment protection laws and high labour costs that reduce the ability of companies to adapt in a rapidly changing environment. Collective bargaining agreements, which can cover entire industries and regions, reduce the flexibility for adjusting wages according to individual company performance or economic conditions.

The loss of competitiveness is reflected in productivity: since 2017 output per worker has dropped 2.5%. These structural problems cannot be reversed rapidly, and they will add to subdued economic performance in the coming years, QNB added.

Business

German economy faces significant hurdles; real GDP expected to remain unchanged in 2024: QNB