The US Federal Reserve seems intent on raising interest rates in the coming months, which QNB said will be the first interest rate increase by the Fed after years of near-zero rates.

Following the Fed’s meeting on June 17, markets are almost evenly split on the date of the lift-off between September and December 2015.

“But there is still considerable disagreement on whether the Fed should be raising rates in the first place. Some argue that with inflation running well below the Fed’s 2% target (the Fed’s preferred measure of core inflation was 1.2% in April), the Fed should at least keep interest rates at their current low levels,” QNB said.

Others disagree with this argument and point out that the unemployment rate of 5.5% is close to the 5-5.2% estimate of the equilibrium rate of unemployment. The Fed, the argument goes, should therefore be raising interest rates soon to prevent the economy from overheating. Who is right in this debate? One way to answer this is to use the ‘Taylor Rule’, named after John Taylor of Stanford University, who first introduced it in 1993. The Taylor Rule is an equation that prescribes the central bank interest rate based on the amount that inflation and unemployment are deviating from their targets.

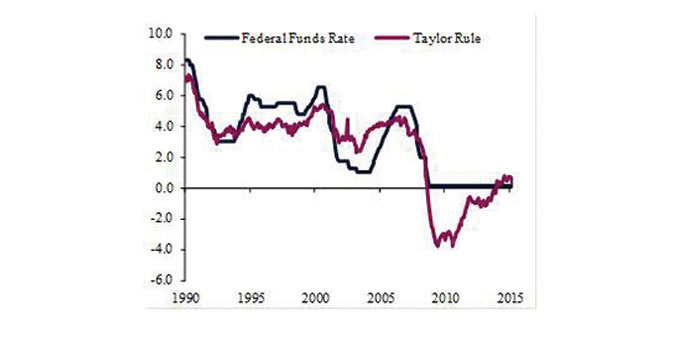

As the chart shows, the Taylor Rule provides a good description of the Fed’s policy rate in the years before the 2008 financial crisis. The chart also highlights the Fed’s dilemma since the crisis, when the rule was recommending deeply negative levels of interest rates.

The Fed could not set interest rates below zero, and resorted instead to unconventional monetary instruments like quantitative easing.

So what is the Taylor Rule recommending now? With inflation at 1.2% and unemployment at 5.5%, the Taylor Rule, which combines both inflation and unemployment to come up with the optimal interest rate, recommends that the Fed’s policy rate should be at 0.36% as shown by the red line in the chart. This is close but slightly higher than the Fed’s current policy range of 0.0-0.25%.

If the Fed’s projections for where unemployment (5.25%) and inflation (1.35%) will be by end-2015 are taken into account, the Taylor Rule recommends that the interest rate should rise to 0.78% by year-end. This is around 0.5% above current policy rate, which is equivalent to two rate hikes. The prediction is in line with the Fed’s forecast that there will be two rate hikes this year.

The Taylor Rule, therefore, is in favour of raising interest rates this year, given the Fed’s baseline forecasts for inflation and unemployment. There are however risks to this view, QNB points out.

First, there is considerable uncertainty about the economy and whether the Fed’s forecasts for unemployment and inflation will be realised. This is especially relevant in light of the weak performance in the first quarter of the year, in which real GDP shrank by 0.2%.

Second, raising rates could spark sharp corrections in the equity and bond markets, which could then have a negative impact on the real economy.

Third, raising rates could trigger capital outflows from emerging markets, which could in turn adversely affect the US through a stronger dollar and lower net exports.

These are all legitimate concerns, but most will probably apply to any time the Fed seeks to raise interest rates. Furthermore, whether a mere 25 basis points hike happens two months early or late is not that important in isolation.

“What is more important is the speed of subsequent rate hikes, as this could make the difference between a rate of 1% or 3% at end-2016 for example. The Fed can easily adjust the speed of rate hikes after the lift-off. It could even reverse some of the tightening if it feels it was premature. “For now, however, the Fed seems intent on raising interest rates in the coming months. Taylor agrees,” QNB said.