Reuters/Jakarta

Investors in Indonesia’s cement-making giants have much to grieve about - blue chips like PT Semen Indonesia Tbk and PT Indocement Tunggal Prakasa Tbk have fallen victim to massive overcapacity, and things are not expected to get better soon.

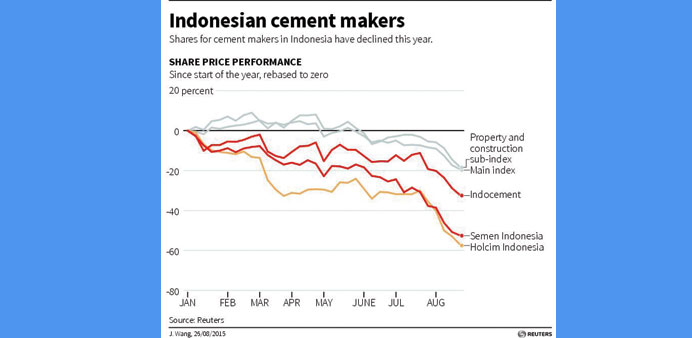

Shares of the country’s largest cement maker Semen Indonesia have plunged 51% so far this year, surpassing the 20% decline in the main stock index. Domestic rivals Indocement and PT Holcim Indonesia Tbk have slumped 33% and 57%, respectively. Some people in the industry say the domestic sales growth outlook this year could be the worst in a decade.

Indonesian cement makers in the last four years have enlarged their production capacity in anticipation of higher demand from infrastructure projects and a property boom. Even Thailand’s Siam Cement Pcl has opened its own cement plant in Indonesia, as well as acquiring a local ready-mix concrete maker, to access the market. China’s Anhui Conch Cement Co Ltd has built a cement plant in Kalimantan and is setting up another in Papua. Indocement itself is majority-owned by Heidelbergcement AG, while Holcim Indonesia is a unit of LafargeHolcim Ltd.

Cement production capacity in Indonesia is expected to rise to 75.5mn tonnes a year by 2016, up about 67% from 2011. Yet demand is far from catching up, with infrastructure spending on roads, bridges and ports delayed by bureaucratic red tape and the economy growing at its slowest pace in six years.

In January-to-June, cement consumption fell 4.3% to 27.7mn tonnes, its worst first-half since 2009, according to industry association data. Heightened competition from new players has not helped. Costs related to transportation in Southeast Asia’s biggest economy have also remained high.

The negative outlook for cement makers has decoupled their shares from property stocks. Both segments of the stock market usually move in tandem, but the plunge in cement counters this year has far exceeded the 18% drop in the sub-index for property and construction. “Property stocks will have more support since price valuation can be justified by more stable valuation of land banks and recurring assets. On the other hand, cement stock valuations are based on cement demand – a less stable variable in the slowing economy and increasing competition,” said Jeffrosenberg Tan, a director with Sinarmas Asset Management who helps manage about 6tn rupiah ($433.53mn) in funds.