Qatar’s current account is expected to turn surplus in 2017 as “oil prices improve and the strong dollar reduces the cost of imports”, a new report has shown.

“We foresee a small current account deficit this year, turning to a surplus next,” said Samba Financial Group in its latest ‘GCC roundup’.

Qatar’s current account moved into deficit ($2.3bn) in the first quarter of 2016. The deficit was caused by a 35% y-o-y fall in the value of exports and a 23% increase in the import bill.

Samba expects a fiscal deficit this year of around 5% of GDP, and 2% in 2017, before the recovery of oil prices allows a small surplus in 2018.

The total deficit over the two years will be around $18bn, which the ministry of finance has stated will be funded entirely by debt issuance, as opposed to drawing down the substantial reserves at the QIA.

Issuance since September 2015 is already at $21.8bn (including the record $9bn international issuance in May of this year). Although the need for fresh capital does not appear particular pressing, the authorities may well decide to take advantage of extremely high international appetite for Gulf debt and make a further issue.

Liquidity remains tight in the banking sector with the loan-to-deposit ratio standing at 115 in June, down slightly on May (118). The improvement in the ratio may have been a result of some of the $9bn in foreign capital the sovereign raised in May finding its way into the local banking system.

Government-related deposits (circa 30% of total deposits) continue to fall, although overall deposit growth is still positive thanks strong nonresident deposit growth. Despite constrained liquidity the government issued $1.3bn of domestic bonds and sukuks in August for which it received offers totalling $2bn.

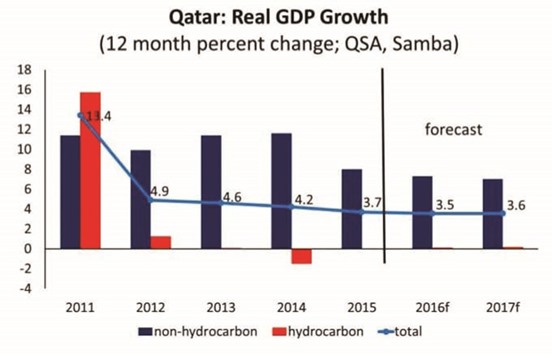

Qatar’s investment spending was the main driver of GDP growth of almost 4% in 2015, with a non-hydrocarbon expansion of 7.8%, partly offset by a contraction in the oil sector. Growth in the first quarter of 2016 came in at 1.1%, with a healthy expansion in the non-hydrocarbon sector (5.5%) dragged down by a 3% contraction in the hydrocarbon sector.

“We expect growth of around 3.5% for 2016 and 2017 as a reduced but still robust level of project spending is supported by a small contribution from the hydrocarbon sector towards the end of this year as the Barzan gas project is commissioned,” Samba noted.